The Legal Deadline May Be 10 August — But the Practical Lending Window Could Close Much Sooner

- Joean Soliman

- 1 day ago

- 4 min read

Floor plans, furniture and fixtures, measurements, and dimensions are approximate and provided for illustrative purposes only.

The recent Federal Government announcement regarding the proposed phase-out of future SMSF lending for residential property has become one of the most significant developments for the SMSF property sector in years. For trustees who have been considering residential property as part of their long-term wealth strategy, the focus has shifted from future planning to taking action. If implemented, the ability to leverage super into residential investment property may become far more restricted, making timing and strategic execution more important than ever.

For investors with 10, 15 or 20 years until retirement, securing this brand-new 3-bedroom townhouse provides the opportunity to build equity, generate rental income and establish a long-term retirement asset while current opportunities remain available.

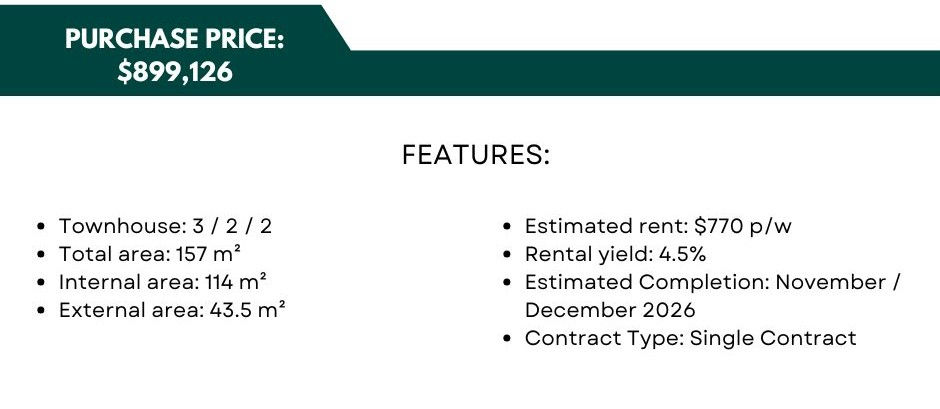

Property Snapshot

Designed to deliver strong rental demand, long-term capital growth and a solid foundation for your SMSF.

Key Detail | The Numbers |

Purchase Price | Brand-New 3-Bedroom Townhouse |

Purchase Price | $899,126 |

Configuration | 3 Bed • 2 Bath • 2 Car |

Total Area | 157m² |

Rental Income | Approx. $770 per week |

Gross Yield | Approx. 4.5% |

Contract | Single Contract |

Estimated Completion | Nov / Dec 2026 |

Why SMSF Investors Are Acting Now

A quality residential townhouse can become the cornerstone of a long-term SMSF investment strategy.

Rental income provides ongoing cash flow, while loan repayments gradually reduce debt and build equity. Combined with long-term capital growth, the property has the potential to become a valuable retirement asset.

Employer super contributions also play an important role. Contributions are based on your income, with the current Superannuation Guarantee set at 12% of ordinary time earnings. For many full-time Australians, this equates to approximately $10,000–$15,000 per year in employer contributions alone, before any additional concessional or personal contributions are made.

When combined with rental income and ongoing loan repayments, these regular contributions can progressively reduce investment debt while strengthening your SMSF's overall equity position.

Contribution amounts are indicative only and will vary based on income, employment arrangements and current superannuation legislation.

A Long-Term Investment Outlook

The table below illustrates how a long-term residential investment may perform over time.

Investment Horizon | Illustrative Property Value* |

Today | $899,126 |

10 Years | $1,610,198 |

15 Years | $2,154,808 |

20 Years | $2,883,619 |

*Illustrative growth scenario only. Actual outcomes will vary based on market performance.

As rental income, employer contributions and loan repayments work together, your investment debt may continue to reduce while equity grows. By retirement, the objective is to own a substantially more valuable asset with significantly lower debt and stronger income potential.

Build Residential First. Diversify Later.

Many SMSF investors are adopting a staged property strategy.

By securing a residential townhouse Today, you can focus on building equity over the next three to five years through capital growth and debt reduction. As your equity position strengthens, you may then be well placed to diversify into commercial SMSF assets such as storage and warehousing, creating multiple income streams designed to support retirement.

Our team can help you build both residential and commercial property strategies, supporting your SMSF through every stage of your investment journey.

Built on Strong Long-Term Fundamentals

This townhouse is supported by key market drivers including continued population growth, infrastructure investment, expanding employment opportunities and sustained housing demand.

Together, these fundamentals continue to underpin long-term capital growth and rental demand, making quality residential property an attractive option for SMSF investors planning for retirement.

Act Before the Window Changes

With proposed changes to future SMSF residential lending now firmly on the agenda, many trustees are choosing to secure quality residential property while opportunities remain available.

Whether your objective is to build equity, reduce debt, create long-term retirement income or position your SMSF for future commercial property investment, this brand-new 3-bedroom townhouse offers an opportunity to establish the foundation of your retirement strategy Today.

The best retirement portfolios aren't built at retirement—they're built years before it.

Important SMSF Update: The Clock Is Now Ticking

The new legislation restricting SMSF borrowing for residential property officially received Royal Assent on 26 June 2026, triggering a 45-day transition period before the changes take full effect.

The Critical Deadline: 10 August 2026

To secure a residential property purchase using an SMSF loan under the current rules, the Contract of Sale must be signed and exchanged on or before 10 August 2026.

Importantly, settlement does not need to occur before this date. As long as contracts are fully executed before the deadline, the purchase should remain protected under the existing rules.

Why Acting Early Matters

While legislation allows purchases up until the 10 August cut-off, there is another major factor investors need to consider: Lender policy changes.

Many banks and specialist lenders are expected to tighten or withdraw SMSF residential lending before the official deadline, meaning access to finance could become more difficult in the coming weeks.

In simple terms: The legal deadline may be 10 August — but the practical lending window could close much sooner.

For investors considering SMSF residential property, timing is now critical.

This info is general and for illustrative purposes only. It doesn't take your personal financial situation into account and isn't intended as financial, legal, or tax advice. Any projections are just a guide based on third-party data. We always recommend checking in with your accountant or a licensed professional before making any investment moves.

+61 485 976 989 | +61 482 080 189

Invest with purpose. Plan with confidence.

Comments